For international businesses dealing with Chinese partners, the annual report (年度报告) is a critical health check. Beyond surface-level financials, it harbors subtle warnings of potential liquidation (清算) – a process that can derail partnerships and investments if missed. Understanding these signals isn’t just prudent; it’s essential for risk mitigation in the complex Chinese market.

Why Liquidation Signals Matter for Foreign Partners

Liquidation in China, governed primarily by the Company Law (公司法, effective July 1, 2024, Articles 229-242) and the Interim Regulations on Enterprise Information Publicity (企业信息公示暂行条例, 2024 Revision, Article 18), signifies a company’s end. It means settling debts, selling assets, and ultimately, dissolution. For foreign entities, this translates to:

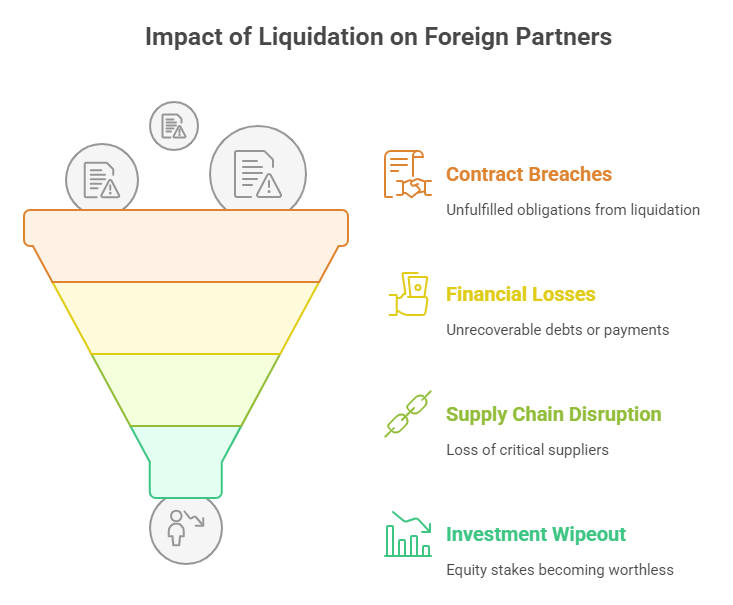

- Breached Contracts: Unfulfilled obligations from a liquidating partner.

- Financial Losses: Unrecoverable debts or advance payments.

- Supply Chain Disruption: Critical suppliers or distributors vanishing.

- Investment Wipeout: Equity stakes becoming worthless.

Official reports, especially the National Enterprise Credit Information Publicity System (NECIPS) Report (企业信用信息公示报告), are legally mandated disclosures. They offer the most authoritative window into a company’s operational and financial standing, including early liquidation flags.

Decoding the “Liquidation Information” Section: The Direct Red Flag

The most explicit signal is found within the NECIPS report under “清算信息” (Liquidation Information).

- “暂无清算信息” (No Liquidation Information Currently): This is the standard, expected entry for an operating company. Its presence alone doesn’t indicate health, but its absence or change is critical.

- Presence of Liquidation Details: If this section suddenly lists details like a liquidation committee (清算组) formation date, appointed liquidators, or contact information for creditors, it’s a definitive, active liquidation warning. This is non-negotiable due diligence failure territory.

Financial Statement Clues: The Silent Alarms

Even without an active “清算信息” entry, the financial data within the annual report can scream instability:

- Persistent & Significant Losses: While startups may lose money, established companies reporting deep, recurring losses year after year, especially with shrinking revenue, signal unsustainable operations. The Company Law (Art. 230) allows shareholders to vote for dissolution if continued existence causes “significant loss” to their interests.

- Vanishing Cash Reserves & Mounting Debt: A critically low cash balance coupled with soaring short-term liabilities (payables, short-term loans) indicates severe liquidity distress. The company may be unable to meet its day-to-day obligations, a precursor to insolvency and forced liquidation (Company Law Art. 231).

- Negative Equity (Owner’s Equity): When total liabilities exceed total assets, the company’s net worth is negative. This is a severe financial crisis point, making voluntary or creditor-initiated liquidation highly likely.

- Abrupt Changes in Asset Ratios: A sudden, unexplained fire-sale of fixed assets (property, plant, equipment) reported in the asset section can indicate desperate attempts to raise cash before collapse.

Operational & Governance Red Flags: Context is Key

Financials don’t exist in a vacuum. Cross-reference them with other report sections:

- Major Scope Reduction: A significant, unexplained narrowing of the “Business Scope” (经营范围) in the “照面信息” section might indicate the loss of core business lines or licenses, crippling operations.

- Frequent, Unexplained Management Turmoil: The “Senior Management Information” (高级管理人员备案) section showing rapid, chaotic turnover of key executives (Directors, Supervisors, GM) often precedes collapse, indicating internal strife or abandonment by leadership.

- Loss of Critical Licenses: For regulated industries, check “Administrative License Information” (行政许可信息). The expiration, non-renewal, or revocation of essential operational licenses can force cessation.

- “Abnormal Operations” Listing: While not liquidation itself, being listed in the “经营异常名录” (Operations Abnormal List) for serious issues (e.g., hiding true financials, fake registered address) is a major reputational blow and regulatory red flag that often precedes deeper failure. The 2024 Information Publicity Regulations (Art. 18) tie this directly to potential deregistration.

- Inability to Contact: Reports may indirectly signal this if the registered address is flagged as invalid or disconnected contact numbers persist. This aligns with conditions for deregistration under the Information Publicity Regulations (Art. 18).

The Legal Trigger: When Dissolution Becomes Mandatory

The Company Law (Art. 229) outlines specific dissolution triggers requiring liquidation:

- Expiry/Trigger: Charter duration expires or a charter-specified dissolution event occurs.

- Shareholder Resolution: Shareholders vote to dissolve.

- Merger/Acquisition: Dissolution required as part of a merger or split.

- License Revocation/Forced Closure: Business license revoked or operations forcibly shut down by authorities.

- Judicial Dissolution: Court orders dissolution due to irreparable management deadlock harming shareholder interests (Art. 231).

Case Study: Spotting the Trajectory (Hypothetical based on common patterns)

Consider “Shenzhen PetroChem Co., Ltd.” NECIPS Report excerpts:

- 2021-2023: Reports show declining revenue, mounting losses, negative equity.

- Jan 2024: Major reduction in registered business scope noted in change record.

- Mar 2024: High turnover in Board and Supervisor positions.

- 2023 Annual Report (Filed Mid-2024): Shows minimal staff (5 employees), near-zero revenue, negative equity exceeding registered capital, cash reserves depleted. “Liquidation Information” still shows “暂无.”

- Potential Path: By late 2024/early 2025, failure to meet obligations could lead to creditor lawsuits, court-ordered liquidation (Company Law Art. 231, 233), or regulatory closure for violations, triggering the appearance of liquidation details in the NECIPS report. The 2024 financials (filed in 2025) would likely confirm the collapse.

Proactive Due Diligence: Don’t Wait for the Obvious

Waiting for the “清算信息” section to populate is often too late. Proactive steps are vital:

- Regular NECIPS Report Monitoring: Obtain and scrutinize the target company’s official NECIPS report annually, comparing year-on-year trends. Look beyond the “Liquidation Info” box.

- Cross-Check Financials: Analyze the “Asset Status Information” (企业资产状况信息) section meticulously for the red flags above (losses, negative equity, liquidity crunch).

- Track Changes: Pay close attention to the “Change Information” (变更信息) log for scope reductions, management chaos, or capital shrinkage.

- Verify Licenses & Status: Ensure critical licenses are valid and the company isn’t listed in the “Operations Abnormal” or “Seriously Illegal” lists.

- Contextualize: Combine report findings with on-the-ground intelligence, news searches, and credit reports for a complete picture.

The Power of the Official Source

While news and rumors exist, the Official Enterprise Credit Report (OECR) from the NECIPS remains the bedrock of credible Chinese corporate intelligence. Its legally mandated disclosures provide the raw data needed to identify liquidation risks early. For international businesses, mastering the interpretation of this report, particularly the interplay between financial distress signals in the annual filings and the legal triggers for dissolution/liquidation outlined in the Company Law, is a non-negotiable component of effective risk management in the Chinese market. Vigilance in reading between these lines can be the difference between a successful partnership and a costly liquidation surprise.

Ensure your due diligence is built on authoritative data. Obtain the definitive Official Enterprise Credit Report directly from China’s National Enterprise Credit Information Publicity System. Explore our full suite of due diligence solutions for the Chinese market on our Services Overview page.

ChinaBizInsight

Your strategic bridge to transparent business in China.